How to Choose Between USDA and Conventional Loans

USDA

Loan vs Conventional Loan:  What’s the Better Option?

What’s the Better Option?

When it comes to buying a home, the USDA loan is one of the most affordable mortgage options for eligible buyers.

Backed by the U.S. Department of Agriculture, this loan program is designed to promote homeownership in rural and some suburban areas. It supports communities that may lack access to affordable housing and helps buyers achieve the dream of homeownership with fewer financial barriers. The USDA initiative also strengthens local economies by boosting residential development in less populated regions.

What Is a USDA Loan?

A USDA loan is a government-backed mortgage available to low- and moderate-income homebuyers who are purchasing in eligible rural areas.

The two main USDA loan programs include:

-

USDA Guaranteed Loan Program: Issued by approved lenders and backed by the USDA.

-

Section 502 Direct Loan Program: Funded directly by the USDA for very low-income households.

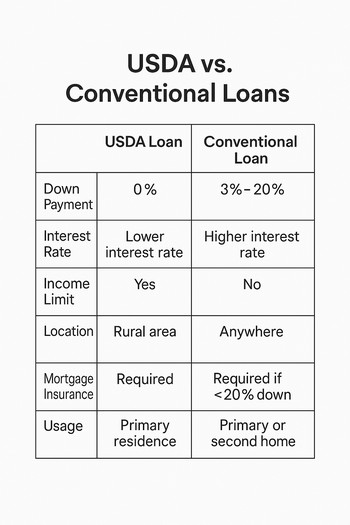

Unlike conventional loans, USDA mortgages come with zero down payment requirements, lower interest rates, and reduced mortgage insurance costs.

USDA loans are particularly attractive to first-time homebuyers and individuals who may not have access to traditional financing due to income limitations or limited savings. The program is designed to help families avoid renting by making homeownership accessible and sustainable.

Benefits of USDA Loans

-

0% down payment: No need for a large upfront investment.

-

Competitive interest rates: USDA loans often offer lower interest rates than conventional loans.

-

Reduced mortgage insurance: USDA charges an upfront guarantee fee and annual fee - usually less than private mortgage insurance (PMI).

-

No cash reserves required: Many lenders do not require reserve funds.

-

Financing for eligible repairs or improvements can be rolled into the loan.

-

Loans are assumable, meaning they can be transferred to a new buyer.

USDA loans also provide more flexible credit requirements compared to conventional options. Many borrowers with limited or no credit history may still qualify with alternative documentation. Additionally, USDA loans support energy-efficient home upgrades, which can help reduce long-term living costs. Some USDA programs also allow for closing costs to be included in the loan, easing the burden on buyers.

Who Can Qualify for a USDA Loan?

To qualify for a USDA loan, applicants must meet specific criteria:

-

Location: The home must be in a USDA-designated rural area.

-

Income: Household income must fall below 115% of the area median.

-

Occupancy: The property must be a primary residence - not a second home or investment.

-

Credit: While there's no hard minimum, lenders typically look for a credit score of 640 or higher.

Applicants must also demonstrate the ability to repay the loan through steady employment and manageable debt levels. USDA loans often use a front-end debt-to-income ratio of 29% and a back-end ratio of 41%. Income documentation, job history, and assets are reviewed closely to ensure long-term affordability.

Conventional Loan: Flexibility for a Broader Market

A conventional loan is a mortgage not insured or guaranteed by the federal government.

It can be a great choice for buyers with strong credit and stable income who may not qualify for a USDA mortgage. Conventional loans are often preferred in competitive housing markets due to faster closings and fewer restrictions.

What Is a Conventional Loan?

Conventional loans are offered by private lenders and follow guidelines set by Fannie Mae and Freddie Mac.

These loans can be conforming or non-conforming depending on whether they meet certain loan limit and underwriting standards. Conforming loans are typically easier to qualify for and offer better rates.

Types of Conventional Loans

-

Fixed-rate mortgages: Monthly payments stay the same over the loan term.

-

Adjustable-rate mortgages (ARMs): Interest rates fluctuate after an initial period.

-

Conforming loans: Follow guidelines set by Fannie Mae or Freddie Mac.

-

Non-conforming loans: Don’t meet the above guidelines - often used for jumbo loans.

Borrowers can also explore portfolio loans through specific banks or lenders that retain the loan rather than sell it. These may offer custom terms or flexibility for unique financial situations. Conventional loans may also include renovation loans for fixer-upper properties, and interest-only loan options for certain investors.

Pros and Cons of Conventional Loans

Pros:

-

More property types: Conventional loans can be used for second homes and investment properties.

-

Flexible loan terms: Common options include 15-, 20-, or 30-year terms.

-

No upfront fees: Unlike USDA, there’s no upfront guarantee fee.

-

Potential to remove PMI: Private mortgage insurance can be canceled once you reach 20% equity.

-

Greater variety of lenders and mortgage products.

-

Stronger refinancing opportunities due to broader lender participation.

Cons:

-

Down payment required: Typically 3% to 20% depending on credit and lender.

-

Private mortgage insurance (PMI): Required if you put down less than 20%.

-

Stricter credit standards: Most lenders prefer scores above 680.

-

Interest rates may be higher for borrowers with lower credit scores or higher debt ratios.

-

May require higher reserves or asset documentation for approval.

FHA Loan: An Alternative to USDA and Conventional

While this article compares USDA and conventional loans, it’s worth briefly mentioning FHA loans.

FHA loans are backed by the Federal Housing Administration and are geared toward buyers with lower credit scores or limited savings. These loans help expand access to homeownership for a wide range of borrowers.

FHA Loan Highlights

-

Low down payment: As little as 3.5% with a credit score of 580 or higher.

-

More lenient credit: Acceptable for borrowers with credit scores in the 500s.

-

Upfront and annual mortgage insurance: Required for all FHA loans regardless of down payment.

-

Assumable loans: Can be transferred to qualified future buyers.

-

Available to buyers in all geographic locations.

-

Allows for higher debt-to-income ratios than many other loans.

FHA loans provide a middle ground - offering easier qualification than conventional loans but without the location restrictions of USDA loans. They are also assumable, meaning a future buyer could take over the loan, potentially saving on interest. FHA loans are especially helpful for buyers with limited credit history or past financial setbacks.

Comparing USDA and Conventional Loans: Key Differences

When comparing USDA and conventional loans, the differences go beyond location.

From interest rates to loan terms, here’s how they stack up:

-

Location Requirements

- USDA loan: Restricted to USDA-eligible rural and suburban areas.

- Conventional loan: No geographic restrictions.

If your desired home isn’t in a qualifying rural area, conventional is the better fit.

-

Down Payment

-

USDA loan: No down payment required.

-

Conventional loan: Requires 3% to 20% depending on the program and borrower profile.

Buyers with limited funds benefit most from USDA’s zero-down feature.

-

Mortgage Insurance

-

USDA: Has a 1% upfront guarantee fee and 0.35% annual fee.

-

Conventional: Requires PMI if under 20% down, but it can be removed when equity reaches 20%.

Over time, PMI on a conventional loan may be cheaper than USDA’s ongoing fees.

-

Credit Score

-

USDA: Most lenders look for 640+, though some accept lower with compensating factors.

-

Conventional: Typically requires 680 or higher for competitive rates.

Conventional loans reward strong credit with better terms.

-

Loan Limits

-

USDA: No official loan limit, but the total loan amount is capped based on income and debt ratios.

-

Conventional: Subject to conforming loan limits ($$806,500 in most areas for 2026).

This can impact your purchasing power depending on the home price and location.

-

Eligible Property Types

-

USDA: Primary residences only. No second homes or investment properties.

-

Conventional: Can be used for second homes, rentals, and vacation properties.

If flexibility is your goal, conventional wins.

-

Property Condition and Use

-

USDA: Home must meet strict safety and livability standards.

-

Conventional: More flexibility on property condition and appraisal criteria.

This is important if you're buying a fixer-upper or unique property.

-

Processing Time and Appraisals

-

USDA: May take longer due to government involvement.

-

Conventional: Typically closes faster and offers more appraisal options.

Faster closings can be a deciding factor in competitive housing markets.

Pros and Cons of USDA Loans vs. Conventional Loans

USDA Loan Pros

-

No down payment required

-

Lower interest rates

-

Easier qualification for low-to-moderate income

-

Great for first-time homebuyers

-

Encourages rural development

-

Can finance closing costs into the loan

-

Flexible guidelines for credit and income

USDA Loan Cons

-

Limited to rural areas

-

Income and location restrictions

-

Annual fee for the life of the loan

-

Only for primary residences

-

May have longer closing timelines

-

Fewer lender options

Conventional Loan Pros

-

Available everywhere

-

Multiple property types allowed

-

PMI can be canceled

-

Greater lender variety

-

Suitable for high-cost areas

-

Offers more customizable loan structures

-

Faster closing timelines

Conventional Loan Cons

-

Requires a down payment

-

Stricter credit and income guidelines

-

Higher rates for lower-credit borrowers

-

PMI costs can be high upfront

-

More sensitive to market interest rate changes

-

May require higher cash reserves

Which Loan Should You Choose?

Choose a USDA Loan if:

-

You want to buy in a USDA-eligible rural or suburban area

-

You need a zero-down option

-

Your household income fits within USDA limits

-

You plan to live in the home full time

-

You want to save on upfront costs

-

You prefer government-backed loan protections

-

You have moderate credit and steady income

Choose a Conventional Loan if:

-

You’re buying outside rural zones

-

You want to purchase a second home or rental

-

You have strong credit and savings

-

You want to avoid government restrictions

-

You’re buying in a high-cost market

-

You want to remove PMI as soon as possible

-

You want more choices in lenders and loan structures

Each loan serves a different borrower profile.

Knowing where you stand financially - and where you want to live - will help you pick the right type of mortgage.

Additional Considerations: FHA and VA Loans

FHA Loan (Quick Review)

-

Designed for low-to-moderate income buyers

-

Flexible credit requirements

-

3.5% down with 580 credit score

-

Mortgage insurance required for the life of the loan

-

Available in all areas

-

Can be combined with down payment assistance programs

-

Ideal for first-time buyers with limited savings

VA Loan

If you’re a veteran, active-duty service member, or eligible surviving spouse, a VA loan could be the best deal of all.

-

0% down

-

No mortgage insurance

-

Competitive interest rates

-

Limited closing costs

-

No loan limits in most areas

-

Includes foreclosure avoidance assistance

-

Can be used to refinance an existing VA or non-VA loan

VA loans often offer the lowest monthly mortgage payment of all. They are a top choice for those who qualify and should always be considered.

Final Thoughts on USDA vs. Conventional Loans

Whether you choose a USDA or conventional loan depends on your unique situation.

USDA loans are ideal for rural, income-qualified buyers with limited savings. Conventional loans suit buyers with stronger financials or those seeking flexibility in location and property type.

Compare lenders, run the numbers, and weigh your long-term goals. No matter which loan you choose, the right option will help you buy a home with confidence.

Consult a trusted loan officer who understands USDA and conventional

guidelines. They can help you explore all options and ensure you secure

the best mortgage for your needs. Don't rush the decision - evaluate all

available programs carefully and choose the path that aligns with your

financial future.

Connect With Us

Please share – it really helps